2/ INFLATION SHOCK

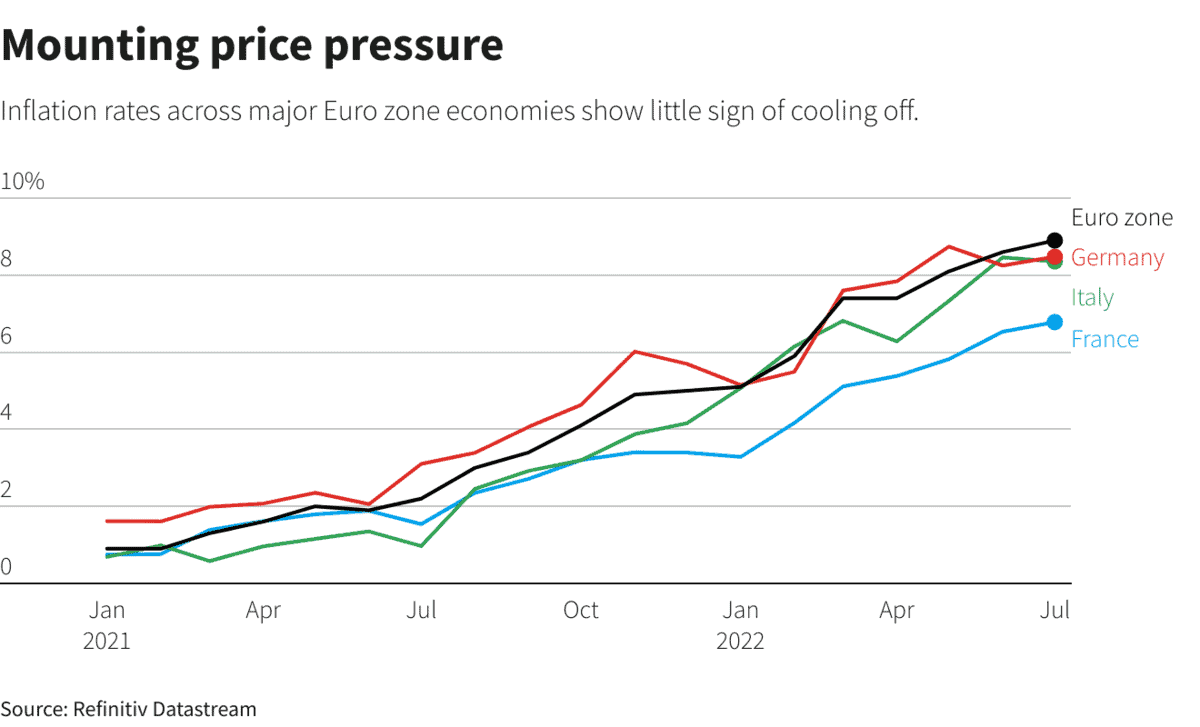

Inflation contained in the euro on-line net web page on-line stays uncomfortably extreme, the flash August shopper mark index on Wednesday is at chance of repeat. That can handiest pile rigidity on the European Central Monetary institution to hike charges however as soon as extra in September similtaneously recession risks mount.

In predicament of peaking shortly, as hoped staunch fairly a couple of weeks contained in the earlier, inflation could shortly hit double digits. It grew to turn into at an annual payment of 8.9% in July – properly above the ECB’s 2% perform.

The availability of distinctive inflation angst is specific: hovering gasoline costs, which lurched larger however as soon as extra as Russia signalled every completely different squeeze on European gasoline affords.

Fuel costs are up 45% in August, and 300% this twelve months. The assemble they perambulate from correct proper right here stays the first to when euro zone inflation will in the end peak. As one economist assemble it, we’re all turning into gasoline watchers now.

2/ INFLATION SHOCK

Inflation contained in the euro on-line net web page on-line stays uncomfortably extreme, the flash August shopper mark index on Wednesday is at chance of repeat. That can handiest pile rigidity on the European Central Monetary institution to hike charges however as soon as extra in September similtaneously recession risks mount.

In predicament of peaking shortly, as hoped staunch fairly a couple of weeks contained in the earlier, inflation could shortly hit double digits. It grew to turn into at an annual payment of 8.9% in July – properly above the ECB’s 2% perform.

The availability of distinctive inflation angst is specific: hovering gasoline costs, which lurched larger however as soon as extra as Russia signalled every completely different squeeze on European gasoline affords.

Fuel costs are up 45% in August, and 300% this twelve months. The assemble they perambulate from correct proper right here stays the first to when euro zone inflation will in the end peak. As one economist assemble it, we’re all turning into gasoline watchers now.

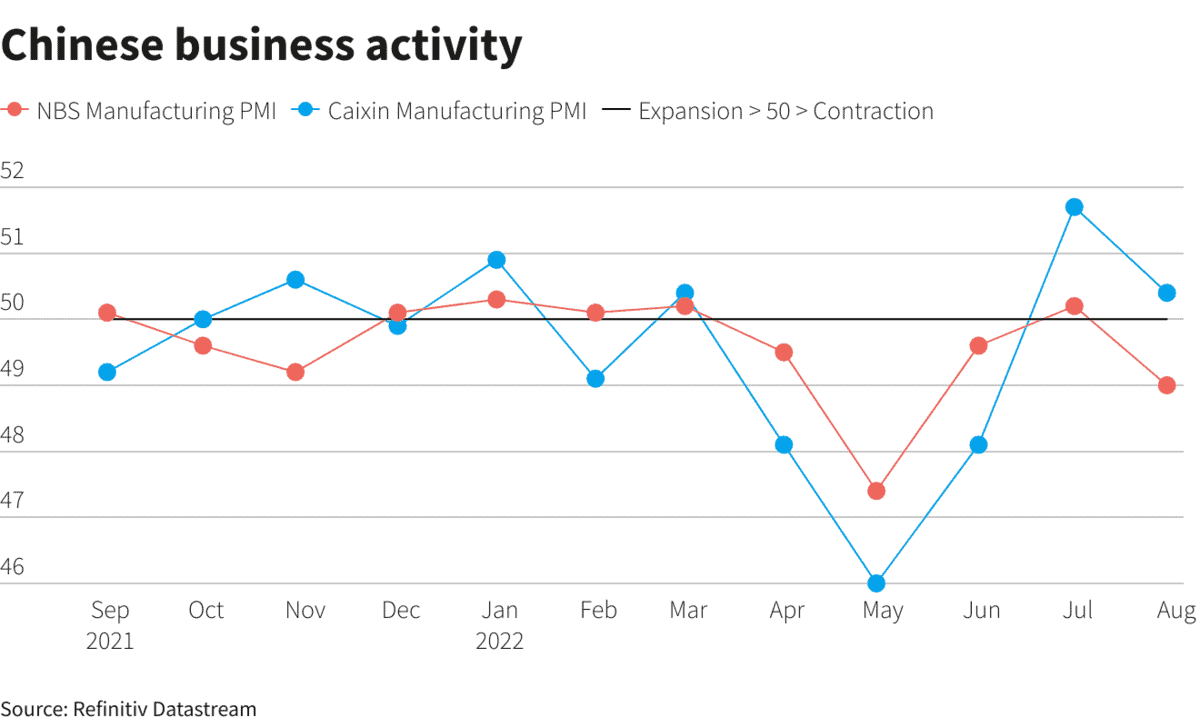

3/ FACTORY FUNK

China’s moribund monetary system will even proceed the lead from the U.S. and Europe in reporting manufacturing gloom inside the upcoming week.

Reliable PMI info for this month is due on Wednesday, after a shock contraction in July as COVID-19 flare-usafuelled by the Omicron variant of the virus compelled additional clampdowns underneath China’s draconian zero-COVID insurance coverage protection insurance coverage insurance policies. The Caixin private spy follows the following day, and is furthermore liable to dipping into contraction territory.

Person and business self perception proceed to be hit by the persevering with property catastrophe. And now a searing heat wave is furthermore hampering manufacturing.

China’s authorities are within the hunt for to salvage enhance this twelve months, with the central financial institution slicing additional lending charges on Monday after slashing others the week earlier than. On Thursday, the authorities launched it'd delay steps to supply a make use of to the labour market, providing the stock market with pretty of cheer.

3/ FACTORY FUNK

China’s moribund monetary system will even proceed the lead from the U.S. and Europe in reporting manufacturing gloom inside the upcoming week.

Reliable PMI info for this month is due on Wednesday, after a shock contraction in July as COVID-19 flare-usafuelled by the Omicron variant of the virus compelled additional clampdowns underneath China’s draconian zero-COVID insurance coverage protection insurance coverage insurance policies. The Caixin private spy follows the following day, and is furthermore liable to dipping into contraction territory.

Person and business self perception proceed to be hit by the persevering with property catastrophe. And now a searing heat wave is furthermore hampering manufacturing.

China’s authorities are within the hunt for to salvage enhance this twelve months, with the central financial institution slicing additional lending charges on Monday after slashing others the week earlier than. On Thursday, the authorities launched it'd delay steps to supply a make use of to the labour market, providing the stock market with pretty of cheer.

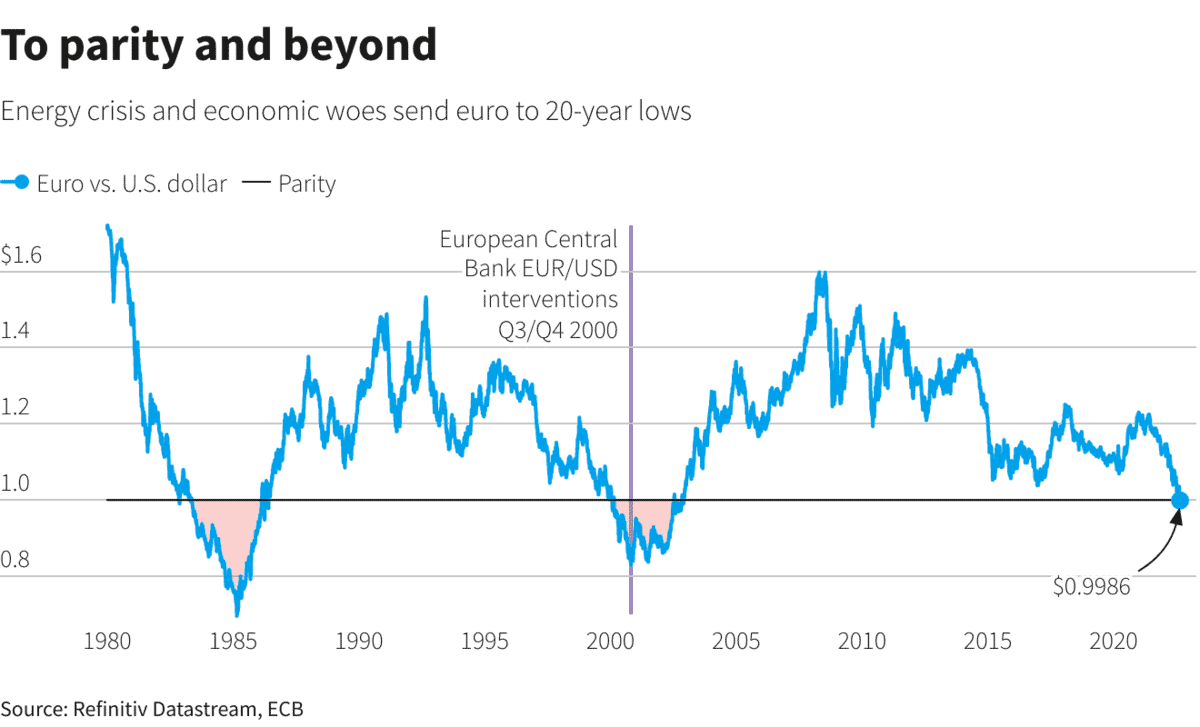

4/BACK BELOW PARITY

Once additional in most fashionable days, one euro grew to turn into worth not as loads as a U.S. buck. The worldwide money’s tumble to distinctive 20-twelve months lows attain $0.99 is emblematic of the scale of the challenges coping with the bloc, not least an vitality catastrophe hitting the euro zone additional troublesome than in several areas.

Yet every completely different dramatic bounce in pure gasoline costs earlier than peak chilly native climate demand in a disclose silent counting on Russian affords is fanning inflation fears, along with expectations the ECB will hike charges sooner similtaneously the monetary system slides inside the route of recession.

Euro/buck is additional and additional correlated with gasoline costs, and patrons and analysts predict additional weak stage as Russia continues curbing its exports.

On a trade-weighted basis, the euro is falling quick too, and solely contained in the near earlier reached its lowest stage since February 2020, when the initiating of the COVID-19 pandemic rattled world markets.

4/BACK BELOW PARITY

Once additional in most fashionable days, one euro grew to turn into worth not as loads as a U.S. buck. The worldwide money’s tumble to distinctive 20-twelve months lows attain $0.99 is emblematic of the scale of the challenges coping with the bloc, not least an vitality catastrophe hitting the euro zone additional troublesome than in several areas.

Yet every completely different dramatic bounce in pure gasoline costs earlier than peak chilly native climate demand in a disclose silent counting on Russian affords is fanning inflation fears, along with expectations the ECB will hike charges sooner similtaneously the monetary system slides inside the route of recession.

Euro/buck is additional and additional correlated with gasoline costs, and patrons and analysts predict additional weak stage as Russia continues curbing its exports.

On a trade-weighted basis, the euro is falling quick too, and solely contained in the near earlier reached its lowest stage since February 2020, when the initiating of the COVID-19 pandemic rattled world markets.

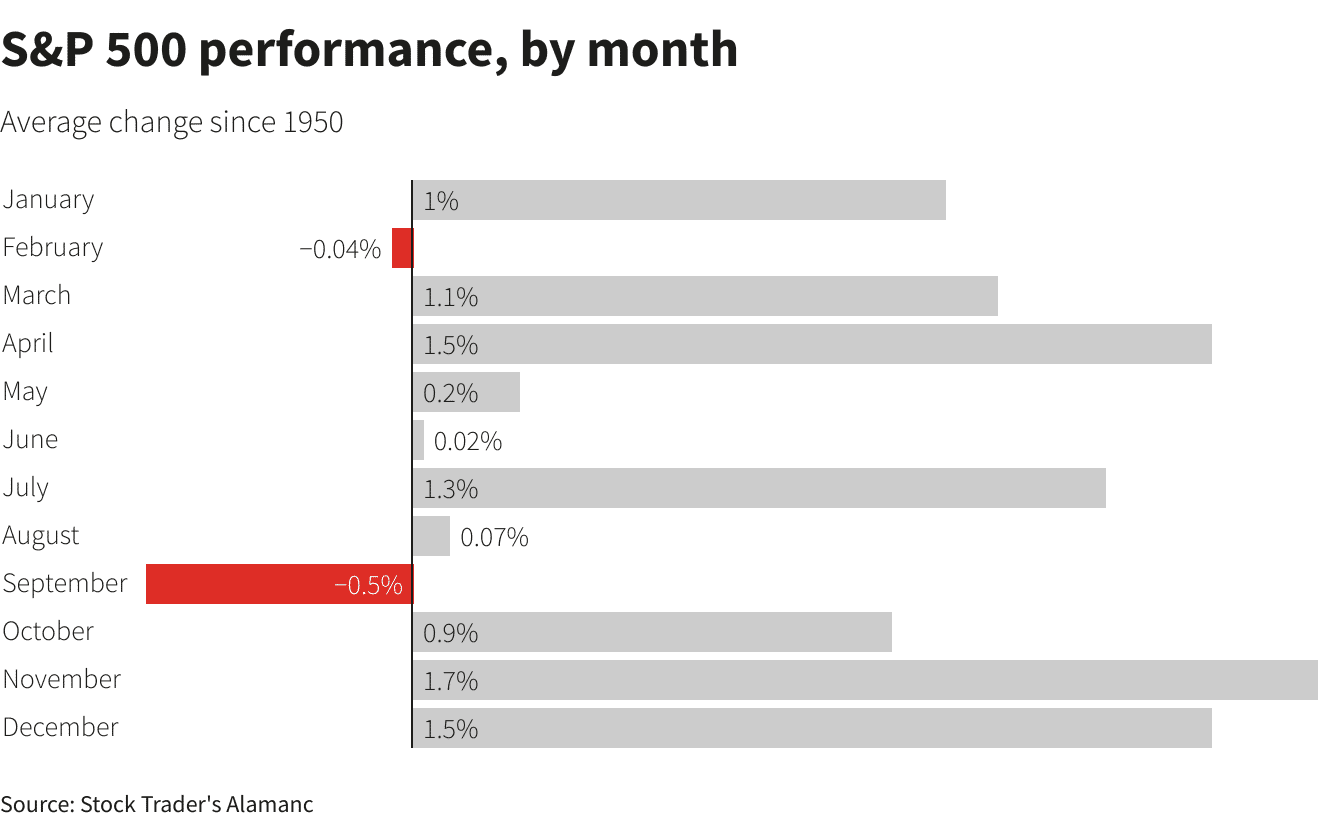

5/STOCKS’ CRUELEST MONTH

The U.S. stock market’s rebound has misplaced some steam, staunch as a result of it is a good distance entering into what has been on common its most treacherous month.

Since 1950, the benchmark S&P 500 has fallen a mean of 0.5% in September, the worst month-to-month effectivity for the index and one amongst handiest two months to register a mean decline, in accordance with the Stock Trader’s Almanac, which notes that fund managers are inclined to advertise underperforming positions as a result of the cease of the third quarter nears.

This September, a selection of factors could place patrons on edge. Following the Jackson Hole central banking symposium in Wyoming, the Fed will retain its subsequent protection assembly on Sept. 20-21. Before that comes principally in all probability essentially the most fashionable finding out on shopper costs that will repeat if inflation has peaked and is at chance of set off volatility no matter the place it lands.

5/STOCKS’ CRUELEST MONTH

The U.S. stock market’s rebound has misplaced some steam, staunch as a result of it is a good distance entering into what has been on common its most treacherous month.

Since 1950, the benchmark S&P 500 has fallen a mean of 0.5% in September, the worst month-to-month effectivity for the index and one amongst handiest two months to register a mean decline, in accordance with the Stock Trader’s Almanac, which notes that fund managers are inclined to advertise underperforming positions as a result of the cease of the third quarter nears.

This September, a selection of factors could place patrons on edge. Following the Jackson Hole central banking symposium in Wyoming, the Fed will retain its subsequent protection assembly on Sept. 20-21. Before that comes principally in all probability essentially the most fashionable finding out on shopper costs that will repeat if inflation has peaked and is at chance of set off volatility no matter the place it lands.

(Compiled by Lewis Krauskopf; Bettering by Paul Simao)

(Compiled by Lewis Krauskopf; Bettering by Paul Simao)

Be taught More